[ad_1]

This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Everyone likes to make fun of Jim Cramer and Mad Money. Well, bad news, Wall Street snobs: his picks are beating the market. Whether that is down to luck or skill we will leave to readers to decide. The show is not bad! Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

More good inflation news

Fewer wild price swings makes inflation forecasting easier. As a result, yesterday’s largely cheery July CPI surprised no one. The headline annual rate nudged up to 3.2 per cent, thanks to base effects, while core inflation slowed to 4.7 per cent. On a monthly basis, the core matched June’s gentle rise of just 16 basis points. The great disinflation in rents and used cars marches on.

A few details. Non-housing core services inflation, or “supercore”, was flat in June, but rose 19bp in July. Blame car insurance and repair inflation (for details, listen to the Unhedged podcast). These reliably hot bits of transportation services more than offset a fall in airfares, which, despite intense volatility, have fully reverted to pre-pandemic price levels and then some:

Several measures of underlying inflation now sport 2-handles. These include: the New York Federal Reserve’s underlying inflation gauge (2.3 per cent); the median CPI component (also 2.3); smoothed three-month supercore (2.1); and trimmed-mean CPI (2.6). These probably overstate the degree of improvement, because they amplify recent changes. But things are undoubtedly better now.

Sustained improvement lets the Fed hold rates steady in September if it wants, buying time to evaluate if inflation will stabilise nearer to 3-4 per cent or 2 per cent.

All eyes remain on the labour market, the hole in the soft landing story. The Atlanta Fed’s wage tracker is at 5.7 per cent, a pace that isn’t historically consistent with 2 per cent inflation. A similar story is under way in job growth, which has slowed significantly, but remains a bit high. Fed economic projections suggest unemployment will have to rise to 4.1 per cent, from 3.5 per cent now, to bring inflation in line. But Carl Riccadonna of BNP Paribas says that historically, unemployment doesn’t begin to increase until monthly payroll growth falls to about 100,000. That could be a few months off:

On top of labour market resilience, Don Rissmiller of Strategas notes that inflation often travels in waves. His chart:

The point is not that the Covid inflation episode is like the others cited above, but that inflation needs to both come down and stay down. This should keep the Fed on notice, and take rate cuts off the table for now.

Omair Sharif of Inflation Insights thinks an inflation bounce could be coming later this year, fuelled by smaller declines in used car prices and a few methodology quirks. “I still can’t rule out a December hike,” he wrote yesterday. Chances are that at the Fed’s December meeting, it will have just seen two hotter core CPI reports in October and November, Sharif says. The latter of those is due out on the first day the Fed meets.

San Francisco Fed president Mary Daly summed it up well yesterday. The July CPI reading “is good news” but “is not a data point that says victory is ours. There’s still more work to do.” (Ethan Wu)

Some replies on Berkshire

A lot of people have opinions about the share performance of Berkshire Hathaway — where it comes from, whether it will persist — and a lot of them wrote in after Unhedged’s piece on that topic earlier this week. To reiterate, despite its recent hot streak, I don’t think Berkshire will ever outperform over a long stretch again, because it is too big and diversified. You might as well own an S&P 500 ETF.

Many of the reader responses were clustered around the broad idea that Berkshire, even if it has not outperformed the S&P over the past decade or more, is in some sense safer than the S&P. Several readers say we should adjust Berkshire’s performance for its large cash position, which acts as a buffer. Here is one of them:

Maybe worth comparing Berkshire to a portfolio of S&P and cash. Berkshire has a cash drag, but has the option to be opportunistic when it becomes a buyers’ market . . . normalising for this by comparing Berkshire to the equivalent “cash & S&P portfolio” would perhaps make for a more appropriate comparison?

I agree that Berkshire’s cash provides optionality, but comparing Berkshire to a blended portfolio of cash and the S&P would be a mistake. The cash position at Berkshire is there to earn high returns opportunistically and to ensure the insurance companies are never caught short of funds. That is a strategic choice by Berkshire designed to improve long-term returns, so to lower the performance benchmark by diluting the S&P performance with cash holdings would be unfair.

Further on the option value of its cash holdings — $147bn as of the second quarter — Unhedged friend Dec Mullarkey of SLC Management writes that:

The other big advantage Buffett has is his ability to act quickly and in size. Given his reputation as a value buyer he is one of the first to get distressed calls. For example, in 2008 when Goldman Sachs and GE needed capital infusions, he stepped in on very favourable terms but passed on Lehman and AIG as saw too many red flags. Companies also seek him out as his analysis and participation enhances credibility, creating a magnet for other investors.

Indeed, the strongest argument for owning Berkshire is that if there is another crisis, it will be able to rent its excess capital out at exorbitant rates and buy up undervalued companies. But Berkshire’s margin of outperformance following the 2008 crisis was very narrow. If you bought Berkshire at the peak of the market in 2007 and held for the next 10 years, your annualised total return would have been 8.6 per cent; the S&P managed 7.3 per cent. That’s a meaningful difference, but nothing like a blowout, given a perfect set-up for Berkshire (and if you had bought Berkshire at the bottom of the market in 2009, you would have undershot the S&P significantly over the next decade).

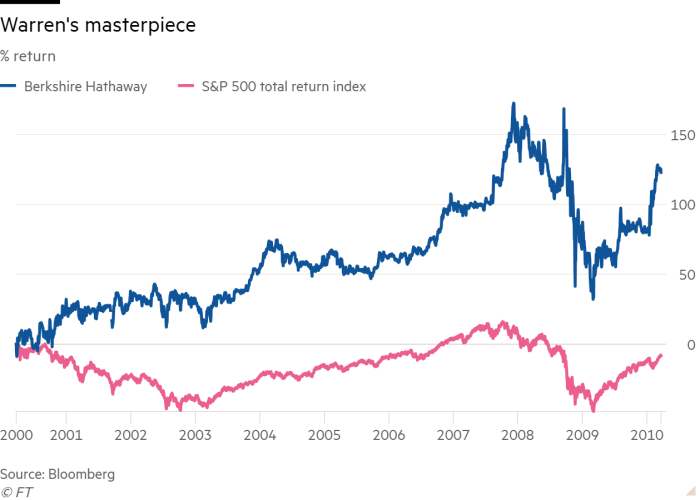

Buffett’s great outperformance came, instead, after the dotcom crash. If you had bought Berkshire at the 2000 peak, you would have earned over 8 per cent a year through the end of 2010, absolutely trouncing the wider market:

Buffett simply didn’t own any tech stocks during the tech bubble (his biggest positions then, in descending order of size: Coke, American Express, Freddie Mac, Gillette, Freddie Mac, Wells Fargo, Washington Post). Is the next crisis likely to miss his portfolio so neatly?

One reader, Michael Kassen, argued that Berkshire’s lower volatility and no-dividend policy create advantages over the S&P:

Let’s assume that over the next 10 years BRK and the S&P produce identical returns. Assuming the future is like the past, investors should prefer BRK as it has a lower beta. Another reason taxable investors should prefer BRK is that there is no tax leakage along the way (versus the dividend component of the S&P returns).

The tax point is right, unless you have to sell the Berkshire shares because you need the money. At that point, it becomes a matter of timing. The beta point is interesting. Berkshire has a beta (volatility relative to the market) of 0.85, according to Bloomberg. Given that, you could in theory lever up your Berkshire position and get higher returns than the S&P for the same risk (where risk is defined in terms of volatility).

Note, however, that Buffett himself thinks that equating risk with volatility is stupid, and that only suckers care about beta. He talks about this a lot. What matters is owning companies that compound high returns over time. Volatility is just a thing that offers investors attractive opportunities to buy or sell.

Another reader suggested that Berkshire might offer greater safety because of superior governance:

One thing to consider is the importance of corporate governance — both ensuring high quality of managers and having appropriate incentives to keep them aligned but not overpaid. Berkshire has excelled at both for decades . . . whereas if you look across the S&P 500 you will always find plenty of examples of poor management or excessive incentives . . . Might that continue to give Berkshire an edge in the future?

I don’t know if Berkshire companies are well governed and managed or not. I can think of only one, Kraft Heinz, that seems to have been badly mismanaged, and one is not very many. But there was the time a senior Berkshire executive “resigned” after he was caught doing something that looked a lot like insider trading. And Berkshire’s disclosures about its privately held businesses are notoriously skimpy. So who knows.

Several readers pointed out the fact that Berkshire has low-cost, embedded leverage in the form of the “float” — premiums paid, but not yet used to pay claims — from its insurance businesses. In short, when Buffett invests the float, he is buying things with borrowed money. The classic statement of this view of Berkshire is a 2013 article from AQR, called “Buffett’s Alpha”. It concludes:

We find that the secret to Buffett’s success is his preference for cheap, safe, high-quality stocks combined with his consistent use of leverage to magnify returns while surviving the inevitable large absolute and relative drawdowns this entails.

After a decade in which this leverage did not lead to outperformance, what are we to conclude? Part of the story could be that Berkshire as a whole has grown faster than its insurance arm, reducing the size of the float relative to the company. I’m not sure, but it is a good subject for further research.

One good read

Bumble is diversifying into the “ecosystem of love”.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, hosted by Ethan Wu and Katie Martin, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.

Recommended newsletters for you

Swamp Notes — Expert insight on the intersection of money and power in US politics. Sign up here

The Lex Newsletter — Lex is the FT’s incisive daily column on investment. Sign up for our newsletter on local and global trends from expert writers in four great financial centres. Sign up here

[ad_2]

Source link

{kind=link}